Context: Indonesia Is Facing a National Waste Emergency

Indonesia's waste management crisis has reached a tipping point that policymakers can no longer defer. The country generates 56.6 million tonnes of solid waste annually, yet 60.9% of it remains improperly managed, disposed of through open dumping or landfills that are nearing full capacity across the archipelago. Without decisive intervention, Indonesia's landfill infrastructure is projected to be exhausted before 2030.

What makes this situation particularly urgent is the track record of previous attempts. Under the old regulatory framework, Presidential Regulation (PR) No. 35/2018, only 2 out of 12 designated cities successfully built Waste-to-Energy (WTE) facilities. More than six major projects in Jakarta alone were suspended or abandoned entirely.

This was not primarily a technical failure. It was a failure of policy design.

Why the Previous Framework Failed

PR 35/2018 contained a structural flaw at its core: a dual revenue model that proved unsustainable in practice. WTE projects were structured to generate income from two sources: a tipping fee paid by local governments, and a feed-in tariff (FIT) of USD 0.13/kWh from the state electricity company PLN. While logical in theory, this arrangement created fiscal complexity that most municipalities simply could not sustain.

When local governments failed to fulfil their tipping fee obligations, often due to limited budget capacity, investors lost revenue certainty and projects stalled. Without a credible, long-term offtake guarantee, commercial lenders were unwilling to provide the project financing these infrastructure developments required.

The core lesson: In large-scale infrastructure projects, institutional complexity is the enemy of bankability.

Five Fundamental Changes Under PR 109/2025

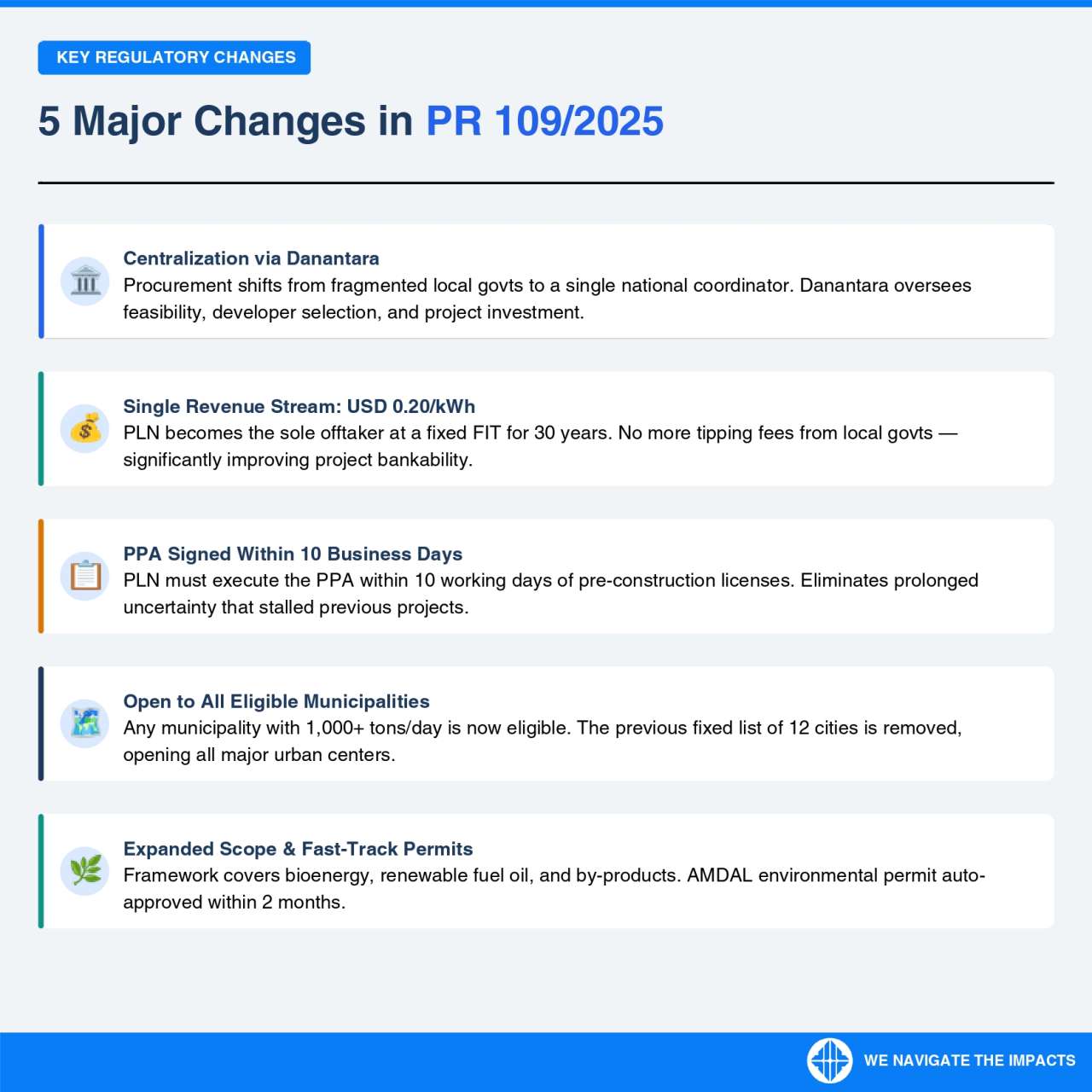

Presidential Regulation No. 109 of 2025 represents a direct and substantive response to the failures of its predecessor. GCG identifies five changes that every stakeholder in this space must understand.

1. Centralization Through Danantara

Project procurement is no longer left to individual local governments, whose capacity, fiscal health, and institutional readiness vary dramatically. Under the new framework, Danantara assumes the role of single national coordinator, overseeing feasibility studies, technical and economic assessments, and developer selection across all eligible municipalities nationwide. This marks a deliberate departure from the decentralized model that demonstrably failed.

2. A Single Revenue Stream at USD 0.20/kWh

PLN is designated as the sole offtaker at a fixed feed-in tariff of USD 0.20/kWh for 30 years. The tipping fee obligation for local governments is removed entirely. With one clear, government-backed revenue stream, the project economics become significantly more attractive to both equity investors and debt financiers.

The increase from USD 0.13 to USD 0.20/kWh is itself a meaningful signal, an acknowledgment by the government that the previous tariff was insufficient to generate the commercial returns necessary to draw serious investment.

3. Power Purchase Agreements Must Be Executed Within 10 Business Days

One of the most persistent bottlenecks under the previous framework was the protracted uncertainty around Power Purchase Agreement (PPA) execution. PR 109/2025 mandates that PLN must sign the PPA within 10 business days of the issuance of pre-construction licenses. This provision directly addresses a timeline risk that had deterred investors from committing to prior projects.

4. Eligibility Extended to All Qualifying Municipalities

The fixed list of 12 designated cities is abolished. Under the new framework, any municipality generating a minimum of 1,000 tonnes of waste per day is automatically eligible to develop WTE infrastructure. This significantly broadens the investment pipeline and distributes opportunity more equitably across Indonesia's urban landscape.

5. Expanded Scope and Accelerated Environmental Permitting

The regulatory framework now extends beyond electricity generation to encompass bioenergy, renewable fuel oil (RFO), and associated by-products. Equally significant, the AMDAL environmental permit is now subject to an auto-approval mechanism within two months, a procedural reform that eliminates one of the most common bureaucratic delays in energy and infrastructure development.

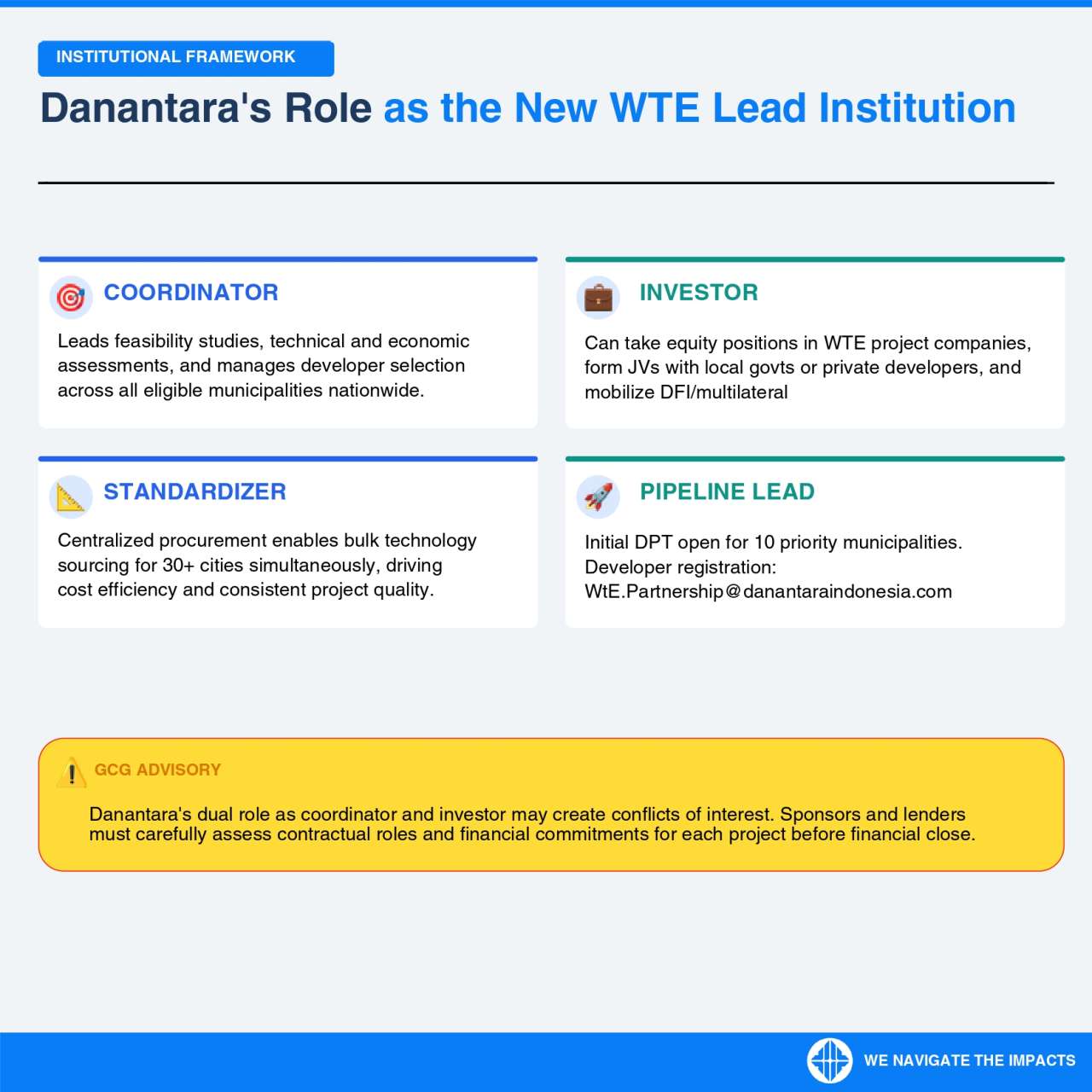

Danantara's Role: Coordinator and Investor

Understanding Danantara's institutional position in its full complexity is essential for any stakeholder navigating this landscape. The agency now simultaneously performs four distinct functions:

- Coordinator: Leads feasibility studies and manages developer selection across all eligible cities

- Standardizer: Centralized procurement enables bulk technology sourcing for 30+ cities simultaneously, creating cost efficiencies and ensuring consistent quality standards

- Investor: Empowered to take equity positions in WTE project companies, form joint ventures with local governments or private developers, and mobilize financing from DFIs and multilateral institutions

- Pipeline Lead: The initial shortlisting process (DPT) is open for 10 priority municipalities.

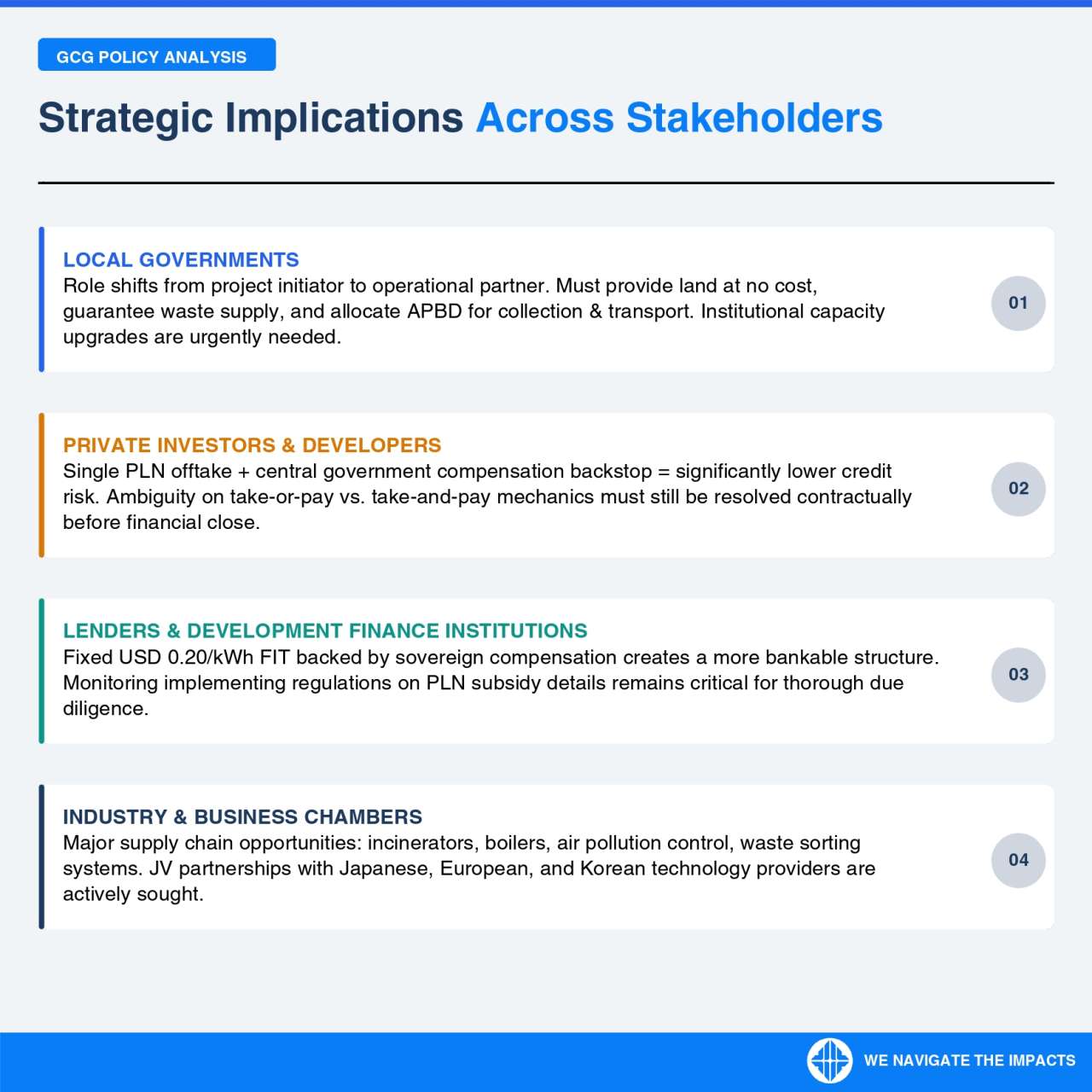

Strategic Implications by Stakeholder

GCG maps the implications of PR 109/2025 specifically across the key stakeholder groups most relevant to this programme.

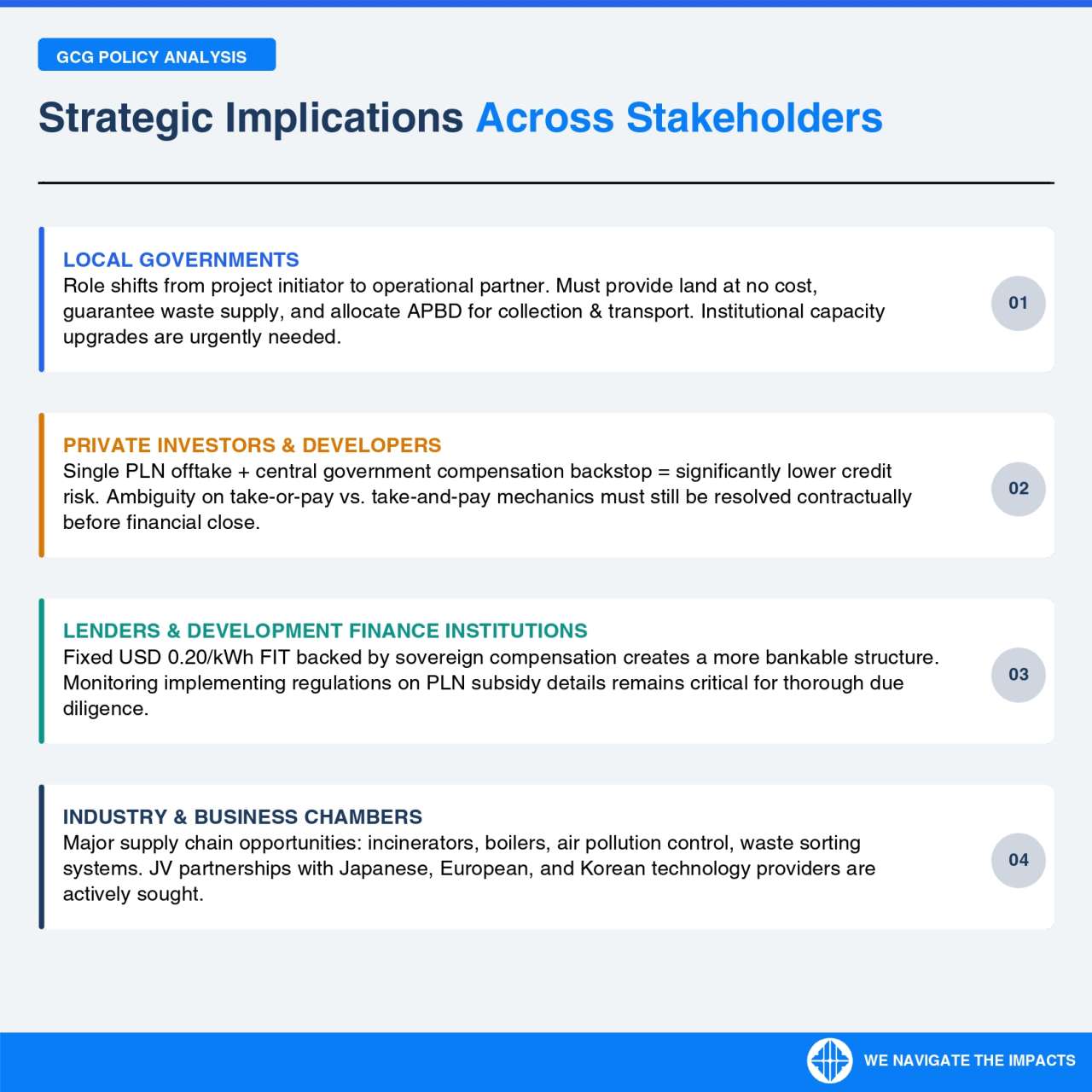

- Local Governments - The role of local government shifts fundamentally, from project initiator to operational partner. Under the new framework, municipalities retain critical obligations: providing land at no cost, guaranteeing a stable waste supply to the facility, and allocating budget (APBD) for waste collection and transport logistics. This shift demands urgent institutional capacity building at the local level, particularly in contract management, cross-agency coordination, and waste data management. Municipalities that invest early in this capacity will be better positioned to attract and sustain projects within their territories.

- Private Investors and Project Developers - The combination of a single PLN offtake arrangement and a central government compensation backstop substantially reduces the credit risk profile of WTE projects compared to the previous framework. This creates significantly more favourable conditions for attracting commercial financing and long-term capital. One critical ambiguity must still be resolved contractually: whether the offtake mechanism operates on a take-or-pay or take-and-pay basis. This distinction has direct implications for revenue certainty and debt service coverage ratios, and must be explicitly addressed in transaction documentation before financial close.

- Lenders and Development Finance Institutions - The fixed USD 0.20/kWh tariff backed by sovereign compensation creates a structurally more bankable project framework than anything previously available in Indonesia's WTE sector. For DFIs and commercial lenders, this is a material improvement. However, monitoring the issuance of implementing regulations — particularly those governing the technical details of PLN subsidy mechanics — remains a critical ongoing task. The quality of the sovereign payment guarantee will ultimately determine the debt serviceability and bankability of individual projects.

- Industry and Business Chambers - The national WTE programme generates substantial supply chain opportunities across multiple segments: incineration technology, industrial boilers, air pollution control systems, and upstream waste sorting infrastructure. The government is actively soliciting global joint venture arrangements, with Japanese, European, and Korean technology providers among those most prominently engaged. For Indonesian industry associations and business chambers, this is also an opportunity to position domestic players as strategic local partners in technology transfer and implementation, a role that can be facilitated through proactive engagement with Danantara's procurement process.

Mapping the Opportunity: Upside and Risk

Conclusion: A Real Window of Opportunity — With Eyes Open

PR 109/2025 constitutes a meaningful and well-structured regulatory improvement. A simplified revenue model, a higher and more commercially viable tariff, and centralized institutional leadership collectively create conditions that are fundamentally different and more investable than those under PR 35/2018.

That said, regulatory momentum alone does not guarantee smooth execution. Municipal capacity constraints, unresolved offtake mechanics, Danantara's potential conflicts of interest, and the pending technical implementing regulations are real variables that every stakeholder must actively manage.

For organisations seeking to participate in this programme, whether as investors, developers, technology suppliers, or local governments, precision in reading the policy landscape and speed in establishing strategic positioning will be the decisive differentiators.